How to create an aggressive savings plan

Pete Zimmerman | 11/20/2022

This post at a glance

( TL ; DR )

If you're in a hurry, you can also hit GO TO VIDEO below

Read time: 10 minutes

Summary: There are a few ways that you can go about saving money. The most common approach is to just put money away when it's convenient. Unfortunately, unless you have a lot of money coming in, a passive game plan like this isn't going to be enough to fuel your goals. For that, you may need an aggressive savings plan. Fortunately, there are some tried and true strategies that can really boost your efforts and slash the time you need to save for your goals.

A bold, aggressive savings plan can clear the way to financial security and comfort

What sounds like more fun to you?

Taking a vacation to a sunny beach, lounging in a cozy chair and sipping mojitos...

or

Letting the $2,500 you didn't spend sit in your bank account, while you creep along through traffic, in the rain, on your way to your 10-hour shift...

Tough question?

Nope, not really.

No one thinks saving is fun. It's no one's idea of a good time. Instead of an aggressive savings plan, you'd probably rather aggressively push your way through the drunks, right up to the swim-up bar.

Understandable...sure. But is it even surprising, then, that almost 20% of people in America don't save any money at all? And most people don't have two nickles to rub together if something bad happens, like their car breaks down or they lose their job?

Spending is fun. But deep down, every adult also understands the importance of saving and preparation. Cashbasic's own surveys show that one of the top priorities for working-class people is financial security and comfort with their money.

So the challenge is this:

Unless you're a trust fund baby, it's impossible to be a free spender and also have security and comfort.

At some point, you have to make a choice.

But once you take that important mental step and decide to act, you have a couple options. You can save passively. Or you can be proactive, and create an aggressive savings plan for yourself.

What's an aggressive savings plan?

Passive saving is easy. All you have to do is save when it's convenient. Have a little extra money left at the end of the month? Go ahead and put it in your rainy day fund. Nothing left at the end of the next month because you had to buy those new baguette slippers? Well, guess there's nothing to save then.

Rinse, repeat.

This is extremely common. And truthfully, it can work. But it isn't the best way if you're really looking to improve. And it can take a long time. Deliberate saving is much more effective.

But it's tough to know where to start with a proactive, aggressive savings plan, and it's much less natural because it runs in a different direction than most people have been taught, and have experienced. It can be hard to power out of that rut.

An aggressive plan means being deliberate instead of passive, and putting your saving first, or at least right near the top of your priority list. It also involves building good habits, crafting a realistic (but effective) plan that works for you, and using smart tactics to keep you on track and help you stick to the plan.

Fortunately, if you're the type of person who would even consider an aggressive savings plan, you're probably also the type who's willing to see it through and put in a little extra effort to make it happen. As a bonus, when you dedicate yourself to learning and growing, your successes and mistakes will both help you make much better, and more informed financial decisions down the road. You can fail forward, so to speak.

So what should you focus on to build an aggressive savings plan?

Keep in mind first that aggressive doesn't always mean fast - zero of the "get rich quick" schemes out there are real. No Nigerian prince is actually sitting there ready to give you your $1 millon inheritance, for zero effort on your part (except sending your bank account information). But you can make real progress with a few simple steps. Read on to learn all about the most important tips to follow.

1: Follow money saving tips and start tracking

Starting to save money can be intimidating. But it's effort well spent, because you can enjoy big benefits of this first step regardless of how well the other steps go. More than almost anything else, learning how to track your money and spending can develop your financial understanding and provide great real-world experience over the long run.

You may have a nagging sense that you do not know where all of your money went at the end of the month, like a persistent little money conscience telling you something that you already know deep down.

Aren't those little nagging feelings usually right?

They don't usually show up telling you that you should have taken one more shot of tequila at the bar, or watched an extra hour of TV instead of going to bed before a long day tomorrow.

Going from a vague sense of your spending to a specific understanding of every transaction you spent money on is a powerful change. One of the great benefits of proactive tracking is that it's going to develop your instincts and positive habits. Each time you see a transaction, and have the chance to think about it and reflect on your decisions, you are training yourself to be deliberate and thoughtful about spending.

Did you really need to spend the money? Was it worth it? Maybe it was, but even taking the time for self-reflection can make you a better steward of your money and life. If you did nothing else, a few months or a year from now, you would have a much better understanding of your spending habits and yourself.

And when you gain this understanding, you'll start to notice when you spend money mindlessly (everyone does it). Even if you are reluctant to give up the things you like spending money on, tracking closely helps you avoid wasting money on the things that bring you the least satisfaction.

Your eyes can start to open to these kinds of saving opportunities and you can start to change your habits, but only if you start by tracking your money in the first place. And eventually, you'll shift to asking those questions before you spend money, instead of just reacting.

Of course, starting to track and follow your finances will help you be successful with the other strategies in this article also. It's actually a prerequisite.

2: Create a reliable money saving guide

More than anything else, creating a budget as soon as possible will help you establish the foundation for your savings plan. But with budgeting, it's critical to be realistic and aggressive at the same time. Almost 3 out of 4 people say they have a budget, but 80% of people also freely admit that they don't stick to it. Usually that's because they've picked a budget that doesn't fit their personality or priorities. You don't want to be that person.

To create your budget/guide, you can start by summing up your inevitable expenses. You might hear these called "required" or "non-discretionary" expenses. Just know that they're the same thing, and would include things like rent, utilities, loan payments, groceries, and similar bills.

Once you have your inevitable expenses down, you'll have to decide what else you will spend money on each week or month. The right amount of spending for you will depend on your own situation.

How much you can (and want to) save

What your personal priorities are and what's important to you

What you will spend your remaining money on (notice that this step comes after you figure out your priorities, not before)

Choosing a budget that works for you, and actually putting it together, is a large topic that can't really be covered here. Check out this article to get everything you need to know about that process and how to be successful with it.

Again, keep in mind that there is no point in having a budget if you will not follow it. Be thoughful and honest with yourself about what you are willing to cut out of your expenses and what you will not. You can always add some aspirational goals on top of everything else. But your initial budget goals should be part of a plan that you personally expect to follow.

3: Put your spending at the end - pay yourself first

Depending on which type of budget you use, you may still have to decide on the order you'll follow when spending your money. You might start by paying for all of your required expenses before moving on to the voluntary expenses. Then plan to keep keep these voluntary expenses low enough to stay within your budgeting goals.

But this sets up a difficult situation when it comes to saving.

Why?

Because one part of you will be fighting to keep your budgetary goals, but another part will be fighting to keep spending money in your usual ways, with your current habits. A sort of financial Jekyl and Hyde.

To sidestep this problem and temptation, you can strive to make saving decisions up front, before spending. That way, you do not have to exhaust your willpower by deciding—over and over again—whether to resist the temptation and save, or to spend a little extra here and there (which adds up quickly).

How do you do this?

By "paying yourself first". Meaning, set a specific savings goal, and set aside that amount as soon as you receive each paycheck. When you do this, savings becomes proactive, and not just a reactive strategy of saving whatever you have left at the end of the month. Reversing the typical, default approach makes it easier for you to think of your remaining money as what you have to work with. Meanwhile, the saved money has already exited to your savings account, safe from impulse buys on Amazon (hey, we all do it).

This psychological change may be just the boost you need to really supercharge your spending goals. But there are also side benefits.

Even if you give in to temptation at the moment and feel like spending a little extra, you'll have to transfer the money out of your savings account first before you plunder it. That may not sound like much, but even this trivial inconvenience and extra step can be enough to make you think twice, and help you stick to your spending goals.

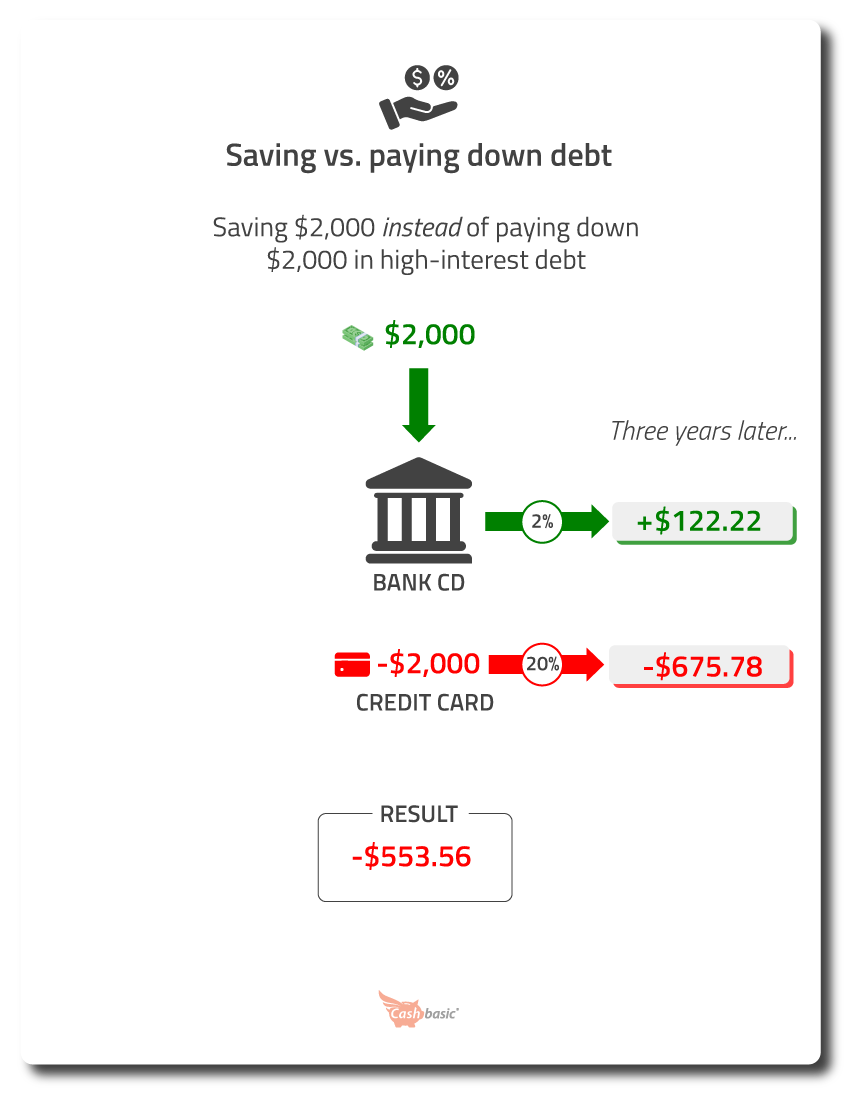

4: Save more money fast by eliminating debt

Most financial goals are admirable—and 1,000 times better than sticking your head in the sand and doing nothing—but some are more effective than others over the long run. For example, unless you're getting a great interest rate, saving money is simply not as efficient as paying off your debt.

Why is that?

Every dollar you save will be yours to keep, and you can usually even earn a little interest on it. But every dollar of debt you pay off will almost always save you more than that dollar over time. Because paying off the debt means freeing yourself from the extra costs of interest payments as well. $2,000 in credit card debt at 20% interest will cost you close to $700 in interest if it takes three years to pay off. That's a lot of money - and money you could be saving.

To take it a little further, the higher the interest on your debt, the higher a priority it should be to pay it off as soon as possible. You might be tempted to tackle your smaller debts first, even if the interest rates on them are lower. And to be fair, there can be a solid psychological boost to scoring an easy win or two and getting rid of those debts and bills. But if you're paying down debt as part of an aggressive plan, the biggest bang for your buck is going to be taking out the most expensive (i.e. higher interest) debt first.

5: Save money fast by slashing expenses

Here's the bottom line when it comes to money:

There are two—and only two—ways that you can move in a positive direction with your money:

- Increase your income

- Lower your expenses

Both of these work. But lowering expenses is almost always easier than earning additional income.

Why?

Two reasons: control and time.

Earning more is great. And candidly, it's a much higher-potential strategy than cutting expenses. There's only so much that can be cut, right? On the other hand, your earning can continue to increase, as you get raises, promotions, or new jobs, or start to take on side gigs for extra income. For max future potential over longer periods of time, earning is where it's at.

But remember, we're talking about an aggressive savings plan. That doesn't mean fast, as we talked about earlier, but it does mean that there's some urgency. And earning more tends to take time. Time to plan, time to ramp up, and time to accumulate. It's also much more difficult for you to control. Maybe you can negotiate a raise here and there. Or you can go get another or different job.

But slashing expenses is fast. You can do it ruthlessly if you put your mind to it, and you can do it today. Right now, while your boss is still thinking through your request (demand?) for a raise.

Here are some solid examples of things that you can cut to reign in spending:

Subscriptions, especially if you don't use them anymore

Routine dining out

High-premium insurance (switch to low-premium, high-deductible)

Impulse buys at the grocery store (schedule your trips and always use a list)

Using food delivery (it isn't free, despite what they try to say)

Other ways to save aggressively and proactively

Mentally prepare yourself to aggressively save money

You will increase your chances of a successful savings plan by getting passionate and excited about your goals. Do whatever it takes to get yourself amped up.

But let's be real...

Personal finance isn't the easiest thing to get excited about. And there's completely relatable reason: money is intangible — you can touch it, but it's really just paper, isn't it? What counts is what money can do for you. So if you want to get passionate about your finances, the best way to do it is to ignore the numbers and accounts, and visualize what you will do with the money once it's saved.

Why are you aggressively saving money? If you are looking to create an emergency fund and build some financial comfort, think about how you'll be able to sleep better at night, stop worrying about money, and start focusing on other things in your life with your newly-found mental space. Are you saving for a wedding? Think about how great your reception will be, and how much fun you'll have with your friends and loved ones.

When you're tempted to buy that new pair of shoes, don't compare it to saving $50 and letting that money sit in your account. Compare it to the alternatives that you're giving up by spending. It's not "shoes vs. saving", it's "shoes vs. peace of mind", or "shoes vs. another $50 towards your beautiful wedding venue".

Get enthusiastic by making your goals for your money real.

It works. Try it.

Earn some money using the money you're saving

Making your money work for you is one of the top principles to learn in personal finance.

Even if you only have a little saved, you can still put those savings to work for you, instead of letting them sit lazily in your checking account. Money market accounts and certificates of deposit ('CDs') usually pay a much higher interest rate than typical checking accounts. And the only major tradeoff is that you may have to give up easy access to the money, since it becomes subject to a lockup. When you're aggressively saving, that's actually a positive, since you don't want to touch that money anyway, right?

Most CDs have a minimum of around $500, so once you've been saving for awhile, they should be a realistic option for you. You can choose how long that you want to hold the CD, and the rate you get paid will apply for that entire period. Those periods (called "terms") are typically three months, six months, one year, two years, three years, or five years. Ask your bank what they have available and they should be more than happy to talk you through it.

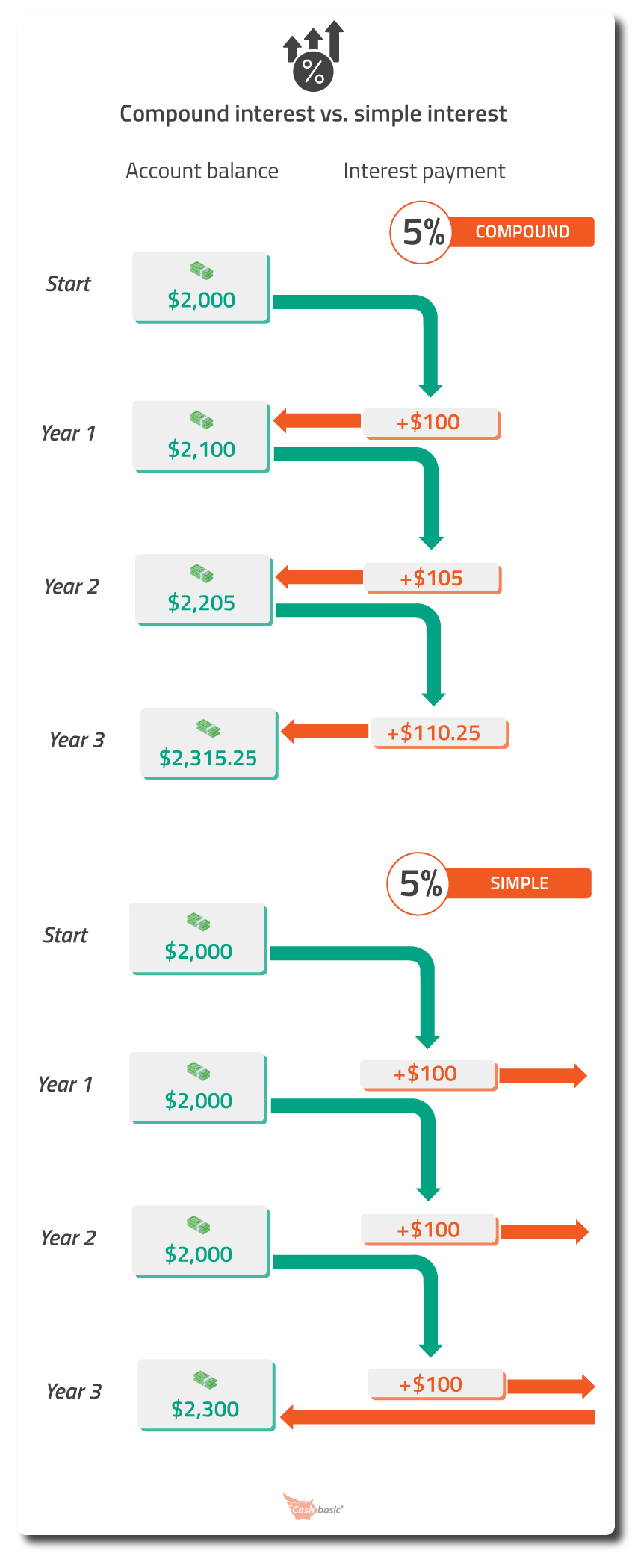

Putting your money to work for you also let's you take advantage of what Einstein called "the eighth wonder of the world": compound interest .

Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn't, pays it.

- Albert Einstein

With compound interest, you earn by getting interest payments on your account balance. Those interest payments are added to your balance, and start to earn money also. Their interest payments start to earn too, and the process repeats. If you've ever wondered how people like Warrnen Buffett made their fortune, this is it.

To be real, you aren't going to become a billionaire overnight by starting to put your money to work for you. But you will earn something, and as a bonus, that money takes itself off the table as a spending temptation also. As your savings accumulate, earning interest becomes a bigger and bigger opportunity. 3% interest on $500 is $15 a year. But 3% on $5,000 is $150. This is a strategy where the potential grows quickly with how much you have saved.

Start your aggressive savings plan today

The more you invest in your aggressive savings plan, the more likely you will be to succceed and start padding your account. The standard, default approach for most people is to save passively, where they can, and a little at a time. But if you're willing to get into it, be proactive, and start to take aggressive action, you can hit your goals much quicker. Want that financial security? Then put your mind to making it happen, instead of waiting for it to come to you (because it won't).

It won't be without sacrifice. Nothing worthwhile is easy. But if you choose a plan that fits your personality and lifestyle, and set realistic expectations and goals, you can start to make progress quickly. Before you know it, you'll have money in the bank and your only regret will be that you didn' start earlier.

Video coming soon...

Share this post

There are no comments yet.

Pete Zimmerman

I've worked in financial services for more than a decade, and know where all the bodies are buried (and where the motivations are). I'm a Certified Financial Planner® and a licensed real estate broker, and love using what I've learned to simplify financial concepts and bring them to life in the real world, for working-class people like you.

Interested in more money ideas and solutions for your life?

Join Cashbasic's mailing list today and get exclusive content and offers direct to your inbox.

Social Connections

Special Thanks

Get Cashbasic's very best content (and exclusive offers) direct to your inbox.

No spam, ever. And we never share or sell your information.